Lots of people decide to finance their purchase of property in Spain with a mortgage. As a foreign buyer of property in Spain the way you can get a mortgage might well be somewhat different than what it is like in your own country. We are going to focus in this article about the differences between getting a mortgage in the USA and Spain because a very high percentage of our clients are from North America and there is a large difference between the systems in the two countries. However, this article will act as a guide for getting a mortgage in Spain: What you will need to supply, what to expect and what sort of outcomes you can expect.

To start off with lets look at what might be a surprising figure for you. The numbers of US buyers in Spain have tripled over the last six years. That number has also meant that each year there are more American buyers looking to finance their purchase too, not least because as prices have risen and interest rates have fallen it makes a lot of sense for many people. However, the system here is different. What you get in the US and what you expect there is not what you find here. There are major differences you need to know and if you don't then you may make major mistakes that can ruin your intended move.

The First Thing To Understand

The most important point to understand is that yes, you can get a mortgage in Spain. However, you must meet certain requirements. Spanish banks actively lend to both resident and non-resident Americans. There are no restrictions on Americans owning property in Spain and no extra taxes are levied on Americans or the vast majority of foreign nationals buying property in Spain. The Golden Visa has gone and buying property doesn't give you residency but you don't need residency to buy and once you have bought and live here then you become a resident. All of the main banks deal with American buyers; Caixabank, Sabadell, BBVA, Santander, Bankinter and even the smaller banks.

The First Shock

The deposit required is likely to be the first main difference between the system in the States and the system here. In the States you might be able to get a mortgage with as little as 3.5% down but usually you need up to 20% of the property cost in your own funds. Here in Spain non-resident mortgages will require you to put down 30-40% of the property price and also the costs of purchase, meaning anohter 14-15% on top. Essentially you need to budget to have at least 40-50% of the property cost with your own funds. The loan to value ratio of 60-70% is normally a non-negotiable. Some banks rarely will give up to 80% for a non resident mortgage but only if you can prove you don't need it of course (Yes, the system favours the rich just like everywhere else) Don't expect 80% as you are unlikely to get it.

Your FICO Score Doesn't Matter

We know you have spent years building up an excellent credit score in the States. It doesn't mean much here! Spanish banks use negative only registries, CIRBE, RAI and ASNEF. If you are on them you won't get credit (Even if you have been placed there erroneously)

You may have an 800 plus FICO score in the States but it means little here. What really does matter is the ratio between your income and your outgoings and your desire over the years to build up a credit score Stateside can actively go against you here. Spanish banks want to see you have no debts, or the fewer the better, and high guaranteed income on a monthly basis (As opposed to savings)

Equally an appalling credit score in the States doesn't necessarily go against you either as long as you have income and little current debt. Good news perhaps.

Banks in Spain look at the following:

- Stability

- Debt to Income Ratio

- Employment Status

- Current Debts

Despite saying this you will be asked for your credit report as a backup check. Experian or Equifax are asked for and expected but Credit Karma and Transunion are NOT generally accepted.

Debt to Income Ratio is Key

The key to getting a mortgage in Spain is your debt to income ratio (DTI). Banks will lend to non-residents so you can get up to 35% of your income on average. Just for the non-maths nerds reading that means if you bring in 10,000 Euros per month then they will lend you enough money to make your maximum repayments on all loans be 3500 Euros. Remember though these repayment criteria include current debt obligations so if you are already paying out, let's say 1500 per month, then they will allow you a payment of up to 2000 Euros more per month on a mortgage.

This means that your mortgage amount and time period to pay off the mortgage may have to be adjusted according to your DTI. As an example let's say that if the bank gave you a 20 year fixed rate mortgage and the repayments would be 2200 Euros per month in that scenario, then they would either ask you to provide a larger downpayment or extend the mortgage period to 25 years in order to bring the repayment down under 2000 per month. Understood?

This means that you often may need to clear some debts before applying for a mortgage here. You may have car loans, student loans, credit card debt and any existing mortgages and they may need to be cleared before applying here. And yes, we know that you only got those debts in order to build your credit score, but here that doesn't matter. This calculation often catches out American clients who may have a high income and lots of savings and investments but their DTI looks terrible. We had a client a couple of years ago who applied for a pre-approval here but was found to have a DTI of 105%!! (They told us by the way after submitting an application) The banks here didn't take into account short term rental incomes he had on investment properties in the States because of one of the things listed above, stability. That could disappear tomorrow so they don't count it. If you want a Spanish mortgage reduce your leverage before applying.

Interest Rates and Loan Terms

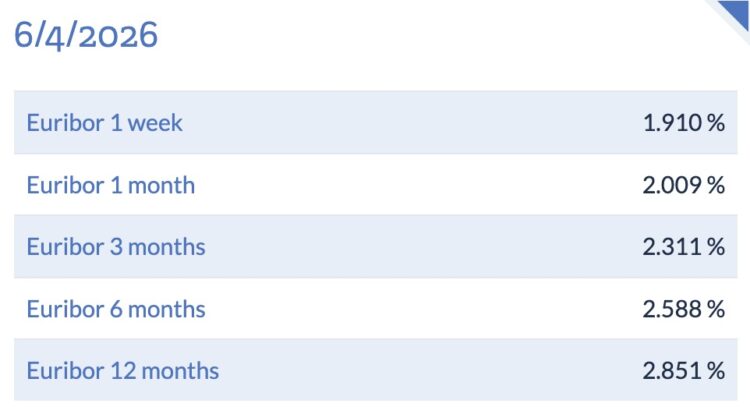

Spain uses the Euribor as the basis for mortgages but not exclusively. Last week we signed for a mortgage at 2.25% fixed rate over 20 years. (The headline rate was 2.95% but there was a discount of 0.7% thanks to having money going into the bank each month, house insurance and bills going through the account) Our on the ground experience recently is a best mortgage of 1.7% fixed rate and a worst case scenario of 3.75% variable, not my favourite but the client profile was more risky for the bank apparently)

The Euribor rates applicable as I write this are below. They change daily

Typically the bank reference is the 12 month rate if you are given a variable rate and there is always a differential, typically Euribor plus 1% after the fixed rate in the first year. However, you don't have to worry about any Euribor changes if you are given a fixed rate mortgage for the whole time period of the loan (Which is standard practice in most cases).

As regards the time period there is something you need to know about and that is that it all depends on your age. The final date for the mortgage term tends to be 75 in Spain now. This means of course that if you are 60 then the maximum term for the mortgage is 15 years not you can get a mortgage if you are 75!

And the last thing to bear in mind regarding mortgages is that interest only mortgages are rare. From the first payment you are paying off capital along with interest.

The Arras Trap

If you haven't got a pre-approval on your mortgage then don't put down a deposit on a property. It's that simple. In the States many sale agreements include a mortgage clause meaning if you are not granted a mortgage then the deposit is returned. That is not the case here (In general) The owner is unlikely to accept your offer and deposit if it is dependent on a mortgage being granted. You can ask but you're likely to be disappointed. They'll just keep it on the market as they don't want to miss someone who may be a cash buyer or who arrives with a pre-approval. If you don't manage to get finance after signing arras (Your 10% deposit) then you will likely lose the deposit with no recourse. Your protection is pre-approval before even visiting properties. That's why we always ask you whether you have it if you are looking for a mortgage and tell you to contact our trusted mortgage brokers to get that all important pre-approval.

This is an important differentiating factor between the US market and the Spanish one and everybody needs to know about it to avoid costly mistakes.

The Paperwork

It's time to sit down and start taking this seriously now. Because once you want to get your pre-approval you'll need to provide some paperwork. The paperwork you need to send to the mortgage company and banks will be different depending on your case.

We have a PDF ready to download for everyone whatever your situation. Are you employed, self employed, retired, have rental income, are a company director or some combination of all of the above? There are common papers needed for all but each category also has its own requirements. You can download the PDF for all mortgage types here but don't get overwhelmed. Only one section is for you, not all of them. If you are not sure which then ask us.

Apart from the paperwork required for the individual mortgage application, as an American you will also need to satisfy US FATCA compliance. FATCA is an overreach of the US government. Your Spanish bank is legally required to collect US tax compliance documents to keep the Don happy. You will need to provide a signed W-9 form, IRS tax transcripts (requested directly from the IRS via irs.gov), and a foreign tax compliance declaration. You should allow 2–4 weeks to gather these before submitting your mortgage application.

Furthermore, once you have opened a Spanish bank account, FBAR obligations (FinCEN Form 114) apply if your combined foreign balances exceed $10,000 at any point during the year. You should consult a US–Spain tax advisor before proceeding and you are lucky there because of course we know people who can do this for you.

What To Do

- Before even looking at a property in real life get pre-approval sorted first, not after you fall in love with something.

- Contact your mortgage provider early and ask for the American document checklist (In case it changes)

- Get a US-Spain tax advisor involved before opening Spanish accounts

- VP's role: we work with mortgage specialists who know this process and we'll keep them up to date with the process of the property purchase in the same way that they will keep us up to date with the progress of the mortgage application.

Who To Work With

Our preferred mortgage broker is Mortgage Direct who we have worked since their inception twenty years ago (The founders were VP clients) They work with all of the major banks and many smaller ones too. They are used to working with non-resident clients and non-standard cases. The rates and conditions they achieve for our clients are excellent. We have no hesitation in recommending them. Fill in the form at this link to get an initial study of your case and to start the process of getting that pre-approval or click on the image below.

Contact Us To Start The Process of Buying in Valencia

Property of the Week

A lovely looking property on a generous plot nestled in the Sierra Calderona with a beautifully maintained lush green garden, cool summer breezes, clean air, nature and total privacy.

This two-storey build has been completely renovated in recent years. On the ground floor, a magnificent shaded porch and seating areas which leads us to a stylish Living-Dining Room with Open-Plan Kitchen, Two Bedrooms, and Bathroom. On the Upper Level a spacious living-dining room with a fireplace (currently used as a bedroom), a Kitchen with Dining Area, Three bedrooms, and luxurious Bathroom.

For all year round comfort the house is equipped with two modern pellet stoves, one on each floor, and a powerful air conditioning unit on the top floor.

Naquera is one of our favourite towns in Valencia, conveniently located with main arteries for the family commute, International schools, a quick drive to the coast and an easy up and down to spend time in the city.

Stepping Stone Rental Property of the Week

Step into what Quality of Life feels like!

We're currently preparing this amazing beach home with ample space to settle in. You're in the ehart of the historic Cabanyal meaning that everything is within walking distance. Fresh produce at the Mercado, most of this beach neighborhood's TOP hangout spots and cafes, grocery stores, pharmacies, etc.

The public Transport (bus and metro) is just on the corner, the metro is 10 minutes away, and chemists, opticians, bike repair, hardware stores, health centre, and even a pretty decent spa are all just around the corner.

The harbour is down the street for boating, sailing, roller blading, strolling, dancing, and tapas! This is quality that you can live in the middle of.

Amazing natural light from all sides. AC in all the rooms, 2 doble bedrooms of which 1 has an ensuite bathroom, and 1 office with a fold-out sofa chair.

Other Things You Should Look At

If you are interested in buying in Valencia then you should also be looking at our other articles all about getting ready. Last week we wrote about payments and you can click on that image below, then make sure to follow through on the other links too to learn more.

What You Need to Pay and When

Buying Valencia Property? Essential Reading

The Podcast: Pets, Payments and Property Renovations

The Ultimate Valencia Property FAQ Compilation